Home Industry E learning What You Need to Know About Te...

E Learning

CIO Bulletin,

29 April, 2026

Author:

Guest

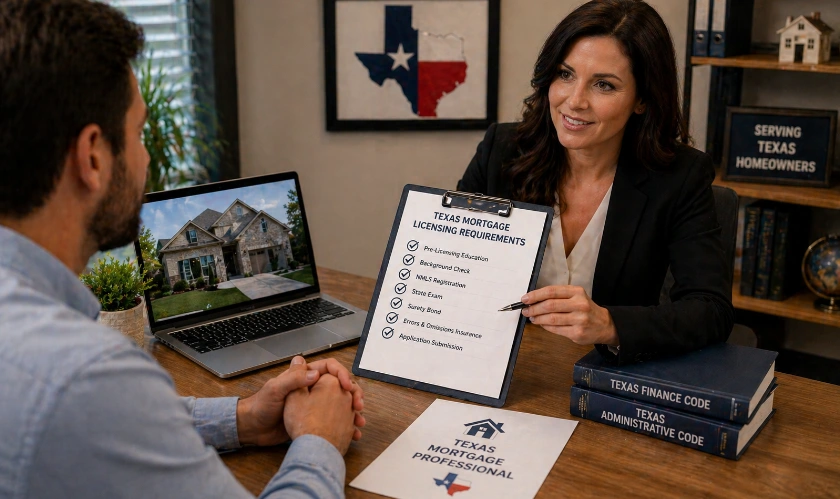

Texas consistently ranks among the hottest real estate markets in the country, and that momentum shows no signs of slowing. For professionals looking to enter the mortgage industry here, proper licensing is not optional. The state enforces a structured process that includes coursework, a national exam, and thorough background screening. These requirements exist for good reason: they protect borrowers and hold originators to a professional standard. Here is a closer look at what the licensing journey actually involves, step by step.

All mortgage loan originators in Texas must register through the Nationwide Multistate Licensing System. This centralized platform handles applications, renewals, and ongoing record management for licensed professionals. The first step is creating an NMLS account and filing Form MU4, which gathers personal information, work history, and responses to specific disclosure questions. Once submitted, the system assigns a unique NMLS identification number. That number follows the individual for the duration of their career in the industry.

Candidates must complete 20 hours of approved pre-licensing education before submitting an application. The curriculum covers federal mortgage statutes, ethical obligations, and core lending principles. Of those 20 hours, three are dedicated to federal law and three to ethics. Two hours are dedicated to non-traditional mortgage products. Earning a Texas mortgage license begins with completing this coursework through an NMLS-approved provider. The remaining hours focus on elective material tied to origination practices and consumer safeguards.

Once the education component is finished, applicants sit for the SAFE MLO Test. The exam includes 125 questions total, though only 120 are scored. A passing score is 75% or higher. Questions cover federal and state regulations, origination procedures, and ethical standards. Those who do not pass on their first attempt can retake the exam after waiting 30 days. If a candidate fails three times, a 180-day waiting period kicks in before they can try again.

Texas requires a criminal background check alongside a credit report review as part of the application. Fingerprints must be submitted through an approved vendor for both FBI and state-level screening. Felony convictions within the prior seven years may result in disqualification, depending on the nature of the offense. Financial history matters too. The credit report should be free of unresolved judgments, tax liens, or repeated patterns of serious delinquency. Reviews are handled on a case-by-case basis, so minor blemishes do not automatically lead to denial.

On top of federal standards, Texas adds its own set of conditions that applicants must satisfy.

A surety bond of $25,000 is required before a license can be issued. This bond acts as a financial safeguard for consumers in the event of fraud or professional misconduct. It must stay active for as long as the license is held.

Individual originators cannot operate independently in Texas. A licensed mortgage company or depository institution must formally sponsor the applicant. That sponsorship is recorded directly through the NMLS during the application stage.

Certain applicants, particularly those seeking company-level licenses, need to demonstrate a minimum net worth. For individual originators, this obligation is typically fulfilled through the sponsoring entity.

Every Texas mortgage license must be renewed before December 31 each year. Renewal hinges on completing eight hours of continuing education annually, covering updates to federal law, ethics standards, and non-traditional lending topics. Missing the deadline results in a lapsed license. Reinstatement after that point may require retaking the national exam and redoing the full pre-licensing education program.

Avoidable errors cause delays for many first-time applicants. Incomplete or inaccurate disclosure answers on Form MU4 top the list of frequent problems. Leaving out past legal issues or financial difficulties can trigger deeper scrutiny or even outright denial. Choosing a course provider that lacks NMLS approval is another costly misstep. Applicants should confirm their education meets official standards well before enrolling. Late fingerprint submissions also slow down the review timeline by weeks in some cases.

Getting licensed as a mortgage originator in Texas calls for careful planning and close attention to every requirement. From completing coursework to clearing background checks, each phase serves a clear purpose in protecting consumers and maintaining industry integrity. Staying organized, meeting deadlines, and double-checking each submission can prevent frustrating setbacks along the way. Those who approach the process with a solid plan will find it far more manageable than it first appears. A valid license opens the door to a stable, rewarding career in one of the busiest lending markets in the country.

consultants ltd.jpg)