Home Industry Compliance and governance 5 Ways AI-Powered Document Aut...

Compliance And Governance

CIO Bulletin,

13 April, 2026

Author:

CIO Bulletin Team

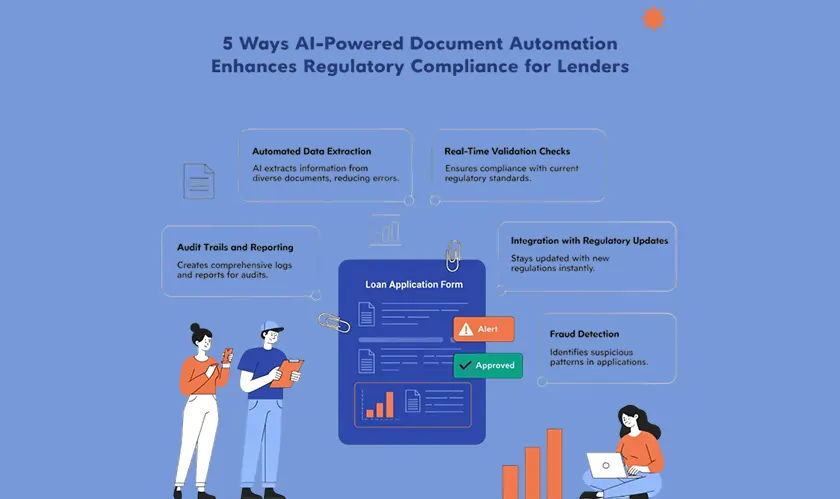

The lending industry works with many changing rules that can feel hard to understand. Banks and other lending places follow these rules to do more than just skip fines. They do it to build trust with people and to run things in the right way. When people check documents by hand, it can lead to mistakes and slow things down. This is now a big problem. A solution is AI-powered automation. This new way of working helps lenders handle data and follow the law in an easier way.

Manual data entry often leads to mistakes, and this can cause big problems with compliance. AI uses advanced Optical Character Recognition (OCR) and machine learning to read data from many forms very well. When you use loan document automation software, lenders can quickly check data across several documents to spot any differences. This helps make sure the data you use for credit checks and reports is checked and right, so you are less likely to run into "fat-finger" mistakes.

Rules such as Truth in Lending (TILA) or Integrated Disclosure (TRID) often change. AI-powered tools can be changed in one place. This lets the whole document process stay up to date.

Fast Rule Changes: You can put new legal rules in the system right away, so people follow them at once.

Live Checklists: Automation tools make real-time lists of what is needed for each loan, in that state or area.

Same Templates: This makes sure every paper and deal uses the newest, approved words.

AI runs on rules that help it find patterns people may not see. It does this by looking at details of each document and watching how people behave. This allows the system to find signs of fraud at the start of the process. This way, lenders can follow rules for Anti-Money Laundering (AML) and Know Your Customer (KYC). These automated checks can check identities right away by looking at worldwide databases. So, every borrower can be checked well, but there is no delay in getting a loan approved.

When people who check rules come by, it is good to have a clear record that shows the order of what happened with a loan. A story of each step helps at this time. AI-powered automation builds a digital “paper trail” for every move made on a document.

Edit Tracking: Records every change made to a document. Shows who made the update and the time it was done.

Time-Stamped Logs: Keep a clear record of when each disclosure is sent. This helps show that all waiting times set by law are followed.

Automatic Exporting: Makes compliance reports fast, in just a few seconds. This helps cut down work before big audits from outside groups.

Compliance is also about keeping important borrower information safe. AI-driven platforms often have strong encryption and set rules about who can see what data. Unlike paper files or scattered digital folders, these systems make sure only the right people see certain information. Keeping things this way helps to meet rules like GDPR or CCPA. It also helps keep the company safe from legal and public problems that can happen if private data gets out.

As the digital world changes, the way that tech and rules come together gets trickier. You can no longer count on using manual steps if you want to keep up and follow the rules. When you use loan document automation software, your bank or credit union can get things done more quickly, make fewer mistakes, and be safer from rule checks. In the end, these tools do more than handle forms. They help set up trust and safety for the lending world we have now

consultants ltd.jpg)